Analys

A moment in markets – The evolving investment narrative surrounding metals

Investors are certainly not oblivious when it comes to expectations of a post-pandemic global economic recovery and the budding chatter about a new commodity supercycle. But the investment narrative for metals is evolving. Due to their growing use in emerging technologies, metals are increasingly being seen as thematic investments.

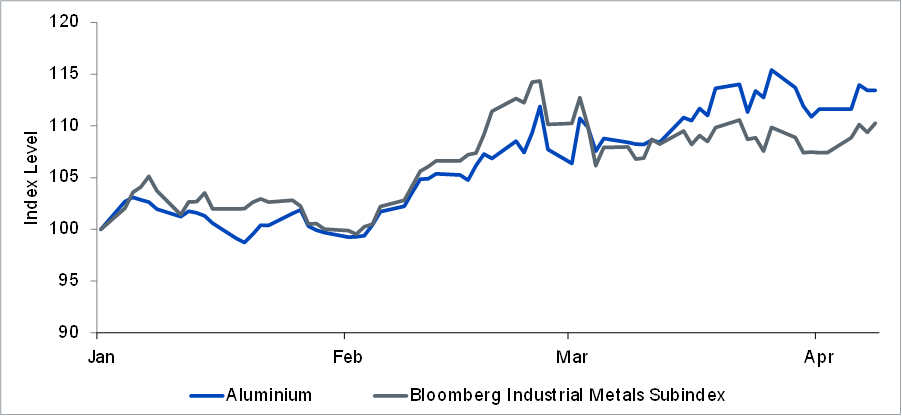

Figure 1: Aluminium prices have outpaced the industrial metals basket recently

For the cyclical upswing

While growing demand from technological megatrends – such as the energy transition – is lengthening the perceived shelf life of metals as investments, cyclical tailwinds do not hurt. In our commodities outlook for 2021, we highlighted four key themes expected to influence commodity prices this year. They include reflation, infrastructure spend driving a structural recovery, an increased focus on the environment, and weather patterns affecting agricultural commodities. The first three have a direct bearing on the outlook for metals.

Reflation relates to a combination of improving industrial demand and accommodative fiscal and monetary conditions. Broad baskets of commodities are favoured within this theme. The pandemic may, however, even encourage governments to start plugging the $15 trillion infrastructure gap to induce economic growth. This can add impetus to the industrial metals sector. Additional support may come from targeted climate focused investment – an example of which is Joe Biden’s $2 trillion plan to build a sustainable clean energy future. While these themes may unfold over the next few years, they are expected to gain more traction in the coming months.

For the megatrends

Industrial metals are the raw materials for many tech related megatrends. There is a growing recognition among investors that equities are not the only way to access these themes. For example, copper’s use in passenger electric vehicles is forecast to rise from less than 0.5 million tonnes (Mt) in 2020 to over 2.5Mt by 2035. The need to build lighter vehicles is also expected to draw higher quantities of metals like aluminium. Similarly, higher loadings of nickel are likely to be used in batteries to power these vehicles. Batteries are expected to account for 30% of nickel demand by 2040 – up from around 5% today. The recent strength in these metals appears to be symptomatic of the growing interest in electric vehicles globally.

Precious metals with industrial applications are relevant to the discussion too. Silver’s use in battery operated electric vehicles ranges between 25-50 grams (g) per vehicle compared to 25-28g for internal combustion engine vehicles. Silver’s automotive demand may rise to 88 million ounces (Moz) by 2025 compared to 51Moz in 2020 as electric vehicles proliferate on the roads. Similarly, if fuel cells are adopted by automakers as a viable source of energy for cars, demand for platinum may rise meaningfully given the metal is used both as a catalyst inside the fuel cell as well as in the production of hydrogen.

Ways to access metals

Investors have options. Exchange traded products typically offer an exposure to front month industrial metals futures. When commodity prices rally sharply, front month exposures generally appear favourable. Enhanced approaches seek instead to maximise the positive roll yield when futures curves are in backwardation and mimimise negative roll yields when futures curves are in contango. The benefits of such approaches are typically seen over longer periods.

When it comes to precious metals, however, many investors prefer physical exposures as precious metals are also perceived as stores of wealth – or providing greater protection against equity and bond market downturns. Silver held in exchange traded products (ETP) currently stands close to record highs of just under 1 billion troy ounces compared to around 0.6 billion troy ounces a year ago. The same is true for ETP holdings of platinum which stand around 3.9 million ounces compared to around 3.5 million ounces a year ago.

The metals mentioned here do not constitute an exhaustive list. They do, however, offer an illustration of how metals are not just for tactical investors interested in the cyclical recovery, but also appeal to long term investors keen to access growing themes in differentiated ways.

By: Mobeen Tahir, Associate Director, Research, WisdomTree