Analys

A moment in markets – Dollar weakness bodes well for commodities

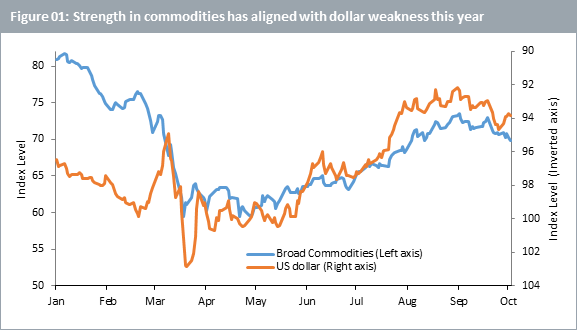

The US dollar has been meaningfully weak this year with most of the depreciation occurring since June. The dollar index spot rate – measured as the average exchange rate between the dollar and major world currencies – fell by over 8% between 15 May and 31 August (see figure 01 below). The US dollar is typically seen as a safe-haven asset during times of financial market volatility and economic uncertainty. This year, however, it has failed to live up to that reputation.

In March, when the pandemic first tightened its grip on markets, the dollar rose sharply but was unable to sustain its gains for long. In September again, as second wave fears and US election uncertainty paired up to create volatility in stock markets, dollar initiated a rebound. It appears to have lost steam even more quickly this time around though.

Weaker for longer?

What else can dollar bulls count on if haven demand fails to materialize despite the challenges facing markets and the economy? Currency strength is relative and weakness in other major currencies including sterling and euro could help revive the dollar. Euro and sterling may fall if Brexit uncertainty and disruption hurt the economic prospects for both Europe and the UK. This would need to be supplemented by continuously improving economic data in the US.

Dollar bears would point to short-term risks facing the economic recovery including second wave virus risks as well as election uncertainty. If the conversation veers towards longer term prospects, they may end up throwing a knockout punch by highlighting the Federal Reserve’s lower for longer policy. In the end, ultra-loose monetary policy for a protracted period is bound to put pressure on the currency.

Commodity investors aren’t complaining

Dollar weakness has helped fuel the recovery rally in broad commodities – albeit supporting different commodity sectors in different ways and to varying degrees. There are two key reasons why dollar weakness supported commodities – notably since June – and why continued weakness in the greenback could be good news for commodity investors:

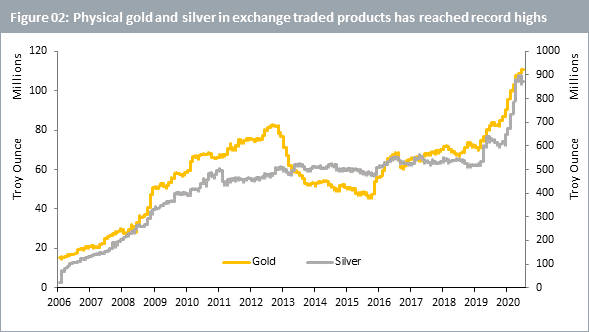

- The haven effect: With the dollar being weak, investors have turned to alternative safe havens as better ‘stores of wealth’. Gold and silver have benefitted the most from this ‘haven effect’. Dollar’s strength and gold’s weakness were both short-lived in March. Investors have turned to physical precious metals knowing that, with their finite supply, they cannot be devalued like fiat currencies by policymakers in response to crises (see figure 02 above).

- The purchasing power effect: Cyclical commodities also benefit from dollar weakness as holders of other currencies find it cheaper to buy dollar-denominated commodities. Both industrial metals and agricultural commodities stand to benefit from this effect.

There is, however, a catch…Trade wars

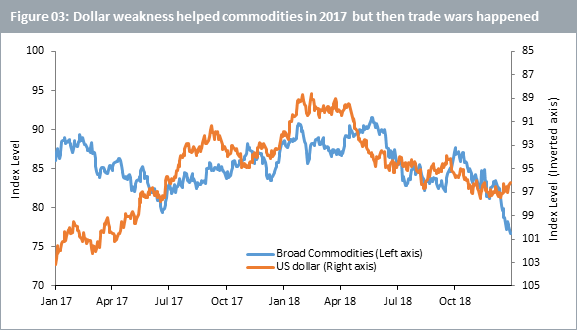

The dollar depreciated considerably in 2017 and start of 2018 which lent support to broad commodities (see figure 03 above). Arguably, among the reasons for the erosion in the currency’s value was an increase in protectionist rhetoric from President Trump. The possibility of the US isolating itself rather than being an integral force in the global economic machine hurt the dollar back then. The reason why commodities could not sustain a lasting rally was because the protectionist rhetoric eventually culminated in a trade dispute between the US and China with tariffs directly imposed on several commodities. While gold benefitted as a geopolitical hedge, cyclical commodities including industrial metals and agriculturals suffered. The catch, therefore, is that for broad commodities to make lasting gains from a weak dollar, the weakness in the currency must stem from accommodative monetary policy rather than an acceleration in trade wars. If trade tensions escalate again, defensive commodities like precious metals will be expected to extend their gains over cyclical sectors.

Mobeen Tahir, Associate Director, Research, WisdomTree