Analys

A man with a moustache is pushing Iran into the corner

Donald Trump’s threat to add 25% tariffs on all Chinese imports is this morning sending Shanghai equities down 6%, S&P 500 futures down 1.7% and Brent crude down 2.1% to $69.4/bl. Over the past year oil and equities have followed each other more or less hand in hand. Brent crude has however traded down close to 9% since its peak on 25 April while the S&P 500 has ticked higher to new all-time highs.

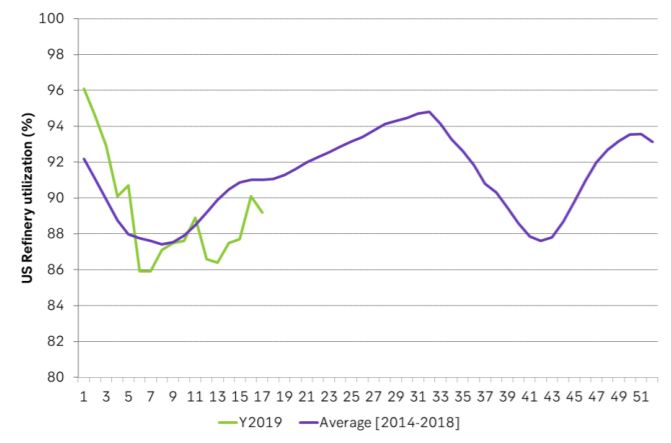

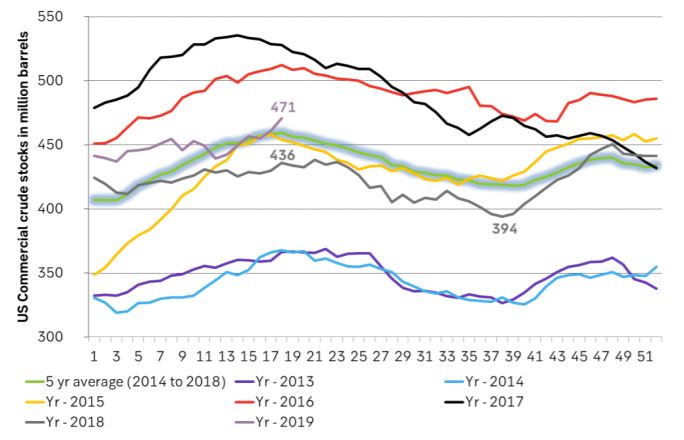

A 31 m bl crude inventory increase in the US since 18 March versus a 5 year normal increase of 15.4 m bl has taken its toll on both WTI and Brent crude. This above normal increase is however easily explained by a 2.2% below normal (5yr average) US refinery utilization rate over the past 7 weeks (since 18 March). This has led to 20 m bl reduced refinery crude processing over those 7 weeks. US crude inventories are actually less above the 5 year average now than they were at the start of the year: 11 m bl now vs 35 m bl above 5yr at the start of the year. US crude, gasoline and mid-dist stocks are right at the 5yr average.

The oil market did get a kick up to $75.6/bl when Donald Trump’s “zero waivers” was announced. Rising US crude stocks (easily explained) has however taken some of the air out of crude prices sending them lower with market placing little concern on Iran and Venezuela with respect to added price.

Oil is selling down this morning with some good reason due to the risk of an escalating trade war between the US and China, but the rise in US crude stocks we have seen since mid-March is not a good reason. This will be reversed as US refineries eventually shifts from below normal utilization to instead above normal utilization.

Now John Bolton (US security advisor) is adding battleship diplomacy to the equation: First maximum financial pressure and distress towards Iran and then he push a gun into their face. The US is now sending the USS Abraham Lincoln carrier strike group to the Gulf. It does however look like this was decided for quite some time ago and that it had the Gulf as a destination on April 1 when it left Virginia in the US. It looks like the presence of aircraft carrier in the US is more about restoring US military presence to normal levels rather than an escalation.

What is rare is however that US security advisor John Bolton is communicating this instead of the Pentagon. He is delivering this as a political decision and move directly linked to US policy linked to Iran and that it is a response to escalating risks in Iran.

John Bolton is a long time Iran hawk and has earlier stated (before White House position) that the only way to stop Iran getting a nuclear weapon is by bombing Iran.

It does look like John Bolton has the initiative with respect to the US policy towards Iran. The positioning of USS Abraham Lincoln in the Gulf may not be a pure military escalation but the message from John Bolton accompanied by it is very uncomfortable.

If this was all about getting pressuring Iran for necessary concessions on the nuclear issues this would not be so bad. Demands from the US on this issue is however not very visible. What are the demands towards Iran on the nuclear issue? European countries have asked for clarity on this issue earlier on in total confusion of what the US is really demanding.

The real uncomfortable sense here is that John Bolton is not after an Iranian nuclear concession but is instead after a regime change. The booming US crude and liquids production has placed the US in a much stronger position to be hard handed towards its political adversaries in for example the Middle East.

A man with a moustache is placing a gun directly into the face of Iran while financially pushing the regime into the corner and the oil market participants should be concerned. Add a price premium. But how much is hard to quantify before it really happens.

Ch1: US crude stocks are up 31 m bl since 18 March vs 5yr normal increase of 15.4 m bl. US crude stocks are now however less above the 5yr normal than they were at the start of the year.

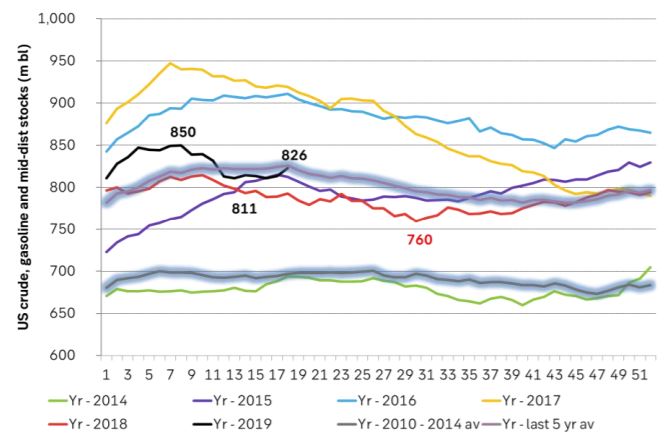

Ch2: US crude, gasoline and middle distillate stocks are slightly higher since its low of 811 m bl but it is at the 5yr average

Ch3: US refinery utilization since 18 March was 2.2% below the 5yr normal. That equates to some 20 m bl less crude processing and is a good explanation for why US crude stocks have risen some 16 m bl more than normal over that period.