Analys

The 2017 crude oil market is starting bullishly but is likely to end modestly as US shale production revives

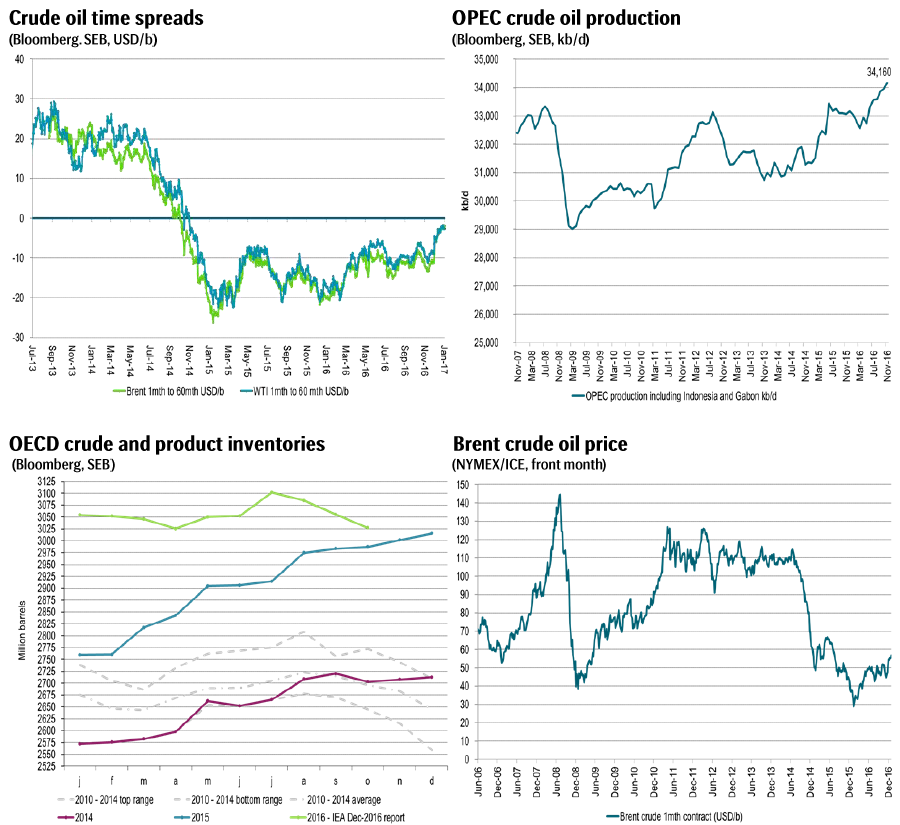

We expect 2017 to be much less dramatic than 2016 unless the supply side is hit by major unforeseen outages. The variations between despair and euphoria should be much less extreme and thus so should the variations in oil prices. While 2016 started bearishly and ended bullishly we expect 2017 to be the opposite but not as extreme. Oil inventories are likely to draw down in H1-17 as OPEC cuts production and crude oil curves are likely to move from deep contango in 2016 to instead backwardation in 2017. While falling in 2016 US shale oil production is going to rise in 2017.

We expect a Brent crude oil price of $55/b in Q1-17, $57.5/b in Q2-17, Q3-17: $55/b, Q4-17: $52.5/b. As a consequence we expect US shale oil rigs to rise by 30 rigs per month in H1-17 (versus 27/mth in H2-16 when Brent crude averaged $49/b) leading total US shale oil rig count to stand at 624 rigs at the start of July 2017. Thereafter there will be no need for additional oil rigs into the US shale oil space before we get to the second half of 2018. Thus by mid-2017 the oil price needs to move to a level which halts further inflow and activation of oil rigs in the US. As such the 12 to 24 month Brent crude oil price probably needs to move down to somewhere between $45-50/b. With crude oil curves having shifted into backwardation with a $5/b spot premium to longer dated contracts it implies a 1 mth Brent crude price of $50-55/b in H2-17.

OPEC has now started to reduce output according to its decision on November 30th to curb output from 34.2 mb/d in November to a planned production of 32.5 mb/d in H2-17. Libya’s crude oil production is however increasing and stood at 685 kb/d this weekend versus an average production of 360 kb/d in 2016. Thus cutting overall OPEC production according to plan is not all without problems. However, Saudi Arabia’s determination as well as its willingness to cut even more than its pledge lends confidence that cuts to overall production will be successful nonetheless. In the face of a further strong rise in US oil rigs during H1-17 we think it will be difficult for OPEC to agree to role forward their production cuts into H2-17. In our view OPEC’s main objective for cutting production in H1-17 is to draw down current elevated global oil inventories thus shifting crude oil prices from a spot discount of $12/b in 2016 to instead a crude oil spot premium of $5/b versus longer dated contracts. We think they will be successful in achieving this with no need to role cuts into H2-17.

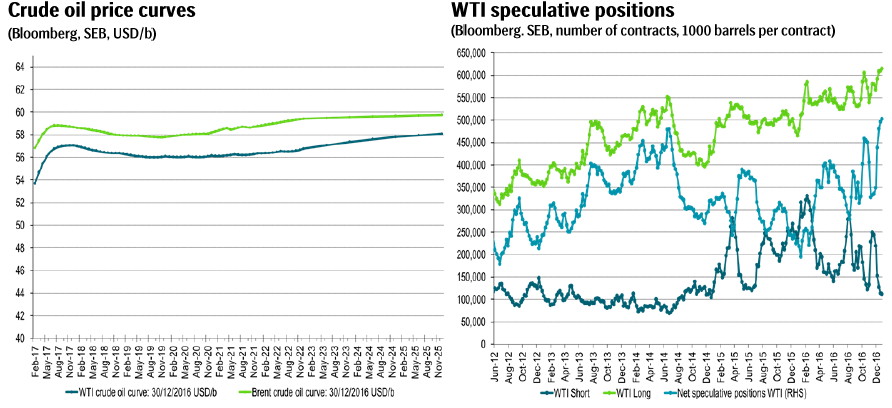

The crude oil market is heading into 2017 on a very bullish note with net long non-commercial WTI positions (i.e. speculative positions) at a record high. The 1mth Brent crude oil price closed the year at $56.82/b which was the highest close since July 2015. US oil producers activated 51 oil rigs in December which was the highest monthly addition since March 2014. With record net long speculative WTI positions and US shale oil rigs on a strongly rising path there is clearly a risk for price set backs ahead even though we have an overall positive view for oil prices in H1-17.

Selected graphs

Kind regards

Bjarne Schieldrop

Chief analyst, Commodities

SEB Markets

Merchant Banking