Analys

Waiting for the next bullish catalyst – but do sell the rally when/if it comes

My key takeaways (Sales Summary)

My key takeaways (Sales Summary)

Oil prices have been volatile lately due to the hurricanes in the U.S Gulf coast, with Brent testing the important support of $53/bbl yesterday, and confirmed it. The Brent front end curve is now again in backwardation. OPEC+ is standing firm on its cuts and they seem open to extending them beyond Q1-18. Oil inventories are declining and the number of US Shale Oil rigs have been declining for four weeks in a row and we believe this trend will continue. US crude production have fallen 700kbbl/d due to hurricane Harvey, which would result in a 5 mbbl outage if it lasts for a week. These factors together with low overall net long speculative positions makes us believe that there is great chance that oil prices will increase during H2. However, spikes should be good opportunities for producers to hedge as we believe there will be plenty of oil in 2018.

Price action – Testing support at $53/b – it held

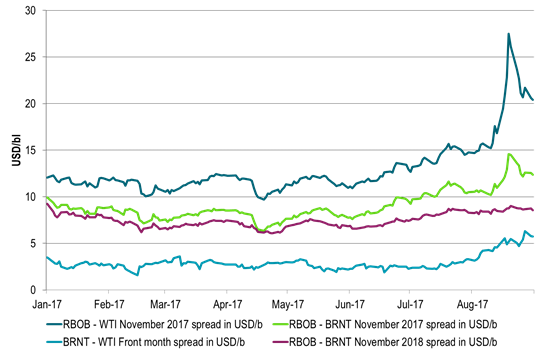

Brent crude traded with some intraday noise yesterday fluctuating between gains and losses before settling up 0.1% on the day at $53.84/b. Intraday it traded down to $53.04/b which seems to have been a pure technical move to test the technical support at $53/b which it recently broke above. Following the price noise from the hurricanes in the U.S. Gulf the Brent crude oil curve is again back in backwardation at the front end of the curve. The WTI curve is however still left in solid contango as the bottlenecks created by Harvey are still problematic. The WTI to Brent November spread has moved out to $5.2/b. The WTI October contract closed up 1.2% ydy as some of the bottlenecks have started to clear but still closed as low as $48.07/b

Crude oil comment – Waiting for the next bullish catalyst – but do sell the rally when/if it comes

Brent crude is back in backwardation at the front of the curve. OPEC+ is standing firm on its cuts. It’s delivering on them and also seems open for extensions beyond 1Q18. Oil inventories are declining and front end crude prices and oil product curve structures are firming.

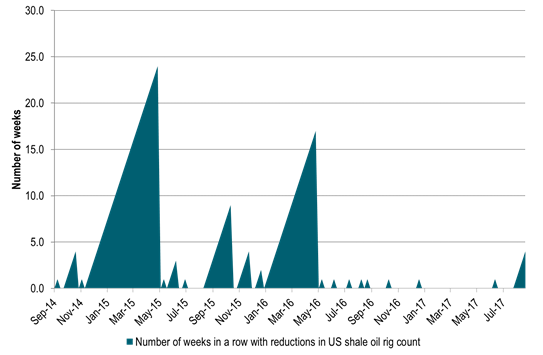

The number of US shale oil rigs declined by 5 rigs again last week to 605 rigs. It has now fallen four weeks in a row which is the first time since May 2016. We think this trend of declining US shale oil rigs is likely to continue towards the end of the year as there are too many rigs with completions struggling to catch up to drilling.

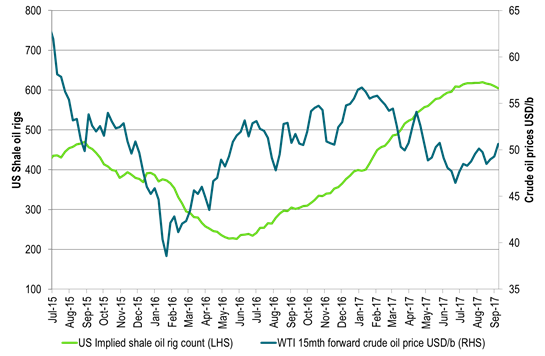

We do not think that this matters too much fundamentally with respect to the oil market balance in 2018 because there is such a large inventory of drilled but uncompleted wells to complete from. For the autumn however we think that seeing the number of drilling rigs declining when the WTI 1-2 year forward prices holds above $50/b could add a positive, bullish sentiment to the oil price: “See, WTI crude is above $50/b and rigs are declining! Shale oil players need a higher price to be profitable!” And maybe they do need a higher price in order to do what they do. That is at least the verdict of equity market which has punished the shale oil sector so far this year in lack of show of profits.

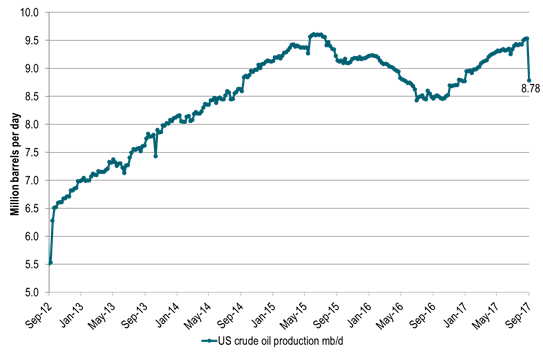

At the moment we also see that that US crude oil production has fallen back some 700 kb/d due to hurricane Harvey. If the outage lasts for a week it will shave 5 million barrels from global oil inventories. However, it will revive and rise strongly towards the end of the year in our view. Thus later in 4Q17 it could take away some of the current optimism of a firming oil market.

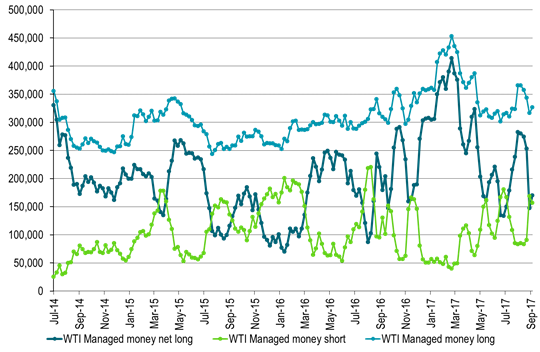

Hedge funds as of Tuesday last week had a fairly low overall net long position. I.e. there is quite a bit of room to the upside in terms of closing down shorts and adding length to their speculative positions.

North Korea has been in the news lately. What would happen to oil if a nuclear event developed is hard to say. For now we have sanctions of oil exports to North Korea on the table. This would of course reduce oil demand and so could be interpreted as potentially bearish. However, the magnitude of their consumption probably does not amount to more than some 20 kb/d. That is no more than the current weekly growth in US crude oil production (baring the recent set-back due to hurricane Harvey).

In the shorter term we have a constructive price situation. OPEC+ is firm on cuts, US shale oil rigs are declining, global oil inventories are declining, US crude production is currently down 700 kb/d, oil production in Libya has recently seen set-backs (though back up again now), hedge funds net speculative positions were at a low level last Tuesday. Technically the Brent crude price has broken up above the important $53/b level. It was tested as support yesterday and it held. Now Brent is set to test the $55.33/b level before the year to date high of $58.37/b (January 3rd) could be challenged.

However, we think there will be plenty of oil in 2018 with the need for OPEC+ to hold cuts through all of next year. Thus a bounce in crude oil prices near term should be utilized as an opportunity to hedged 2018 for the natural sellers, the producers. A new round of hard hitting hurricanes approaching the U.S. Gulf thus creating supply disruption risks could be the catalyst for such a bounce. A new and slightly longer set-back in Libya’s crude oil production could be another one. Producers and natural sellers should stay ready to utilize such a bounce.

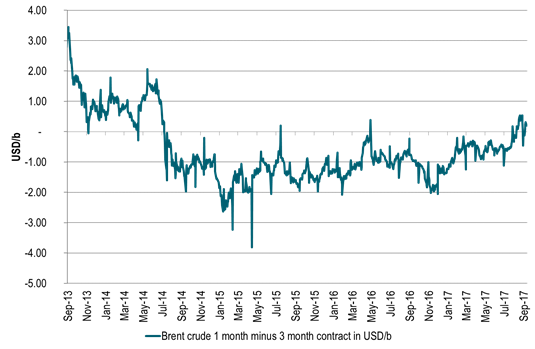

Ch1: Brent crude front end curve back in backwardation

We have not had a lasting backwardation like this since 2014

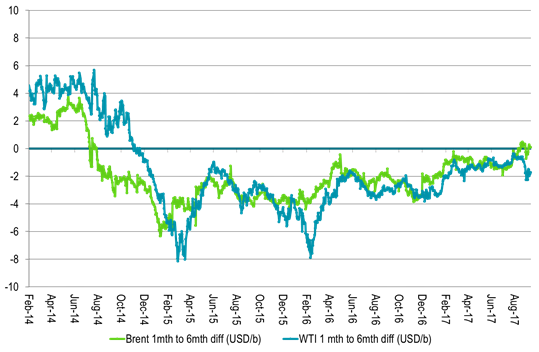

Ch2: The WTI crude curve is still in contango however. Clogged with bottlenecks from hurricane Harvey

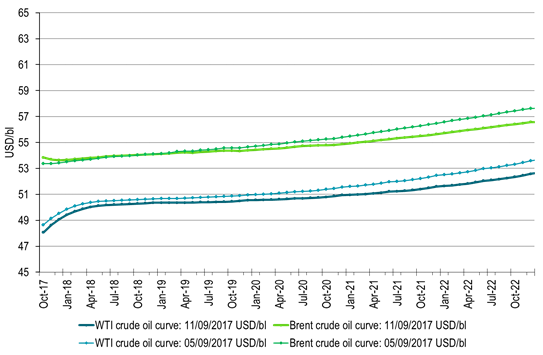

Ch4: Crude oil forward curves now and one week ago

Ch5: Hedge funds net long spec at low level as of Tuesday last week

Room to add length which would give bullish impetus to oil prices

Ch6: The spike in product cracks created by hurricane Harvey have fallen back

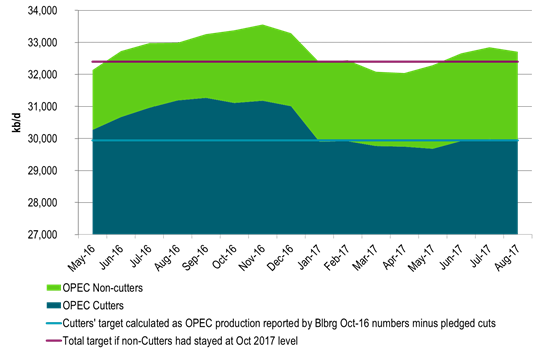

Ch7: OPEC is delivering on its pledge cuts

Ch8: US implied shale oil rigs have fallen back 4 weeks in a row – first since May 2016

Ch9: US implied shale oil rigs falling back

Ch10: US crude oil production disrupted some 700 kb/d by hurricane Harvey

Shaving some 5 mb off global inventories if it lasts for a week

Kind regards

Bjarne Schieldrop

Chief analyst, Commodities

SEB Markets

Merchant Banking

In the past two trading days, Brent Crude prices have fluctuated between highs of USD 92.2 per barrel and lows of USD 88.7 per barrel. Despite escalation tensions in the Middle East, oil prices have remained relatively stable over the past 24 hours. The recent barrage of rockets and drones in the region hasn’t significantly affected market sentiment regarding potential disruptions to oil supply. The key concern now is how Israel will respond: will it choose a strong retaliation to assert deterrence, risking wider regional instability, or will it revert to targeted strikes on Iran’s proxies in Lebanon, Syria, Yemen, and Iraq? While it’s too early to predict, one thing is clear: brace for increased volatility, uncertainty, and speculation.

Amidst these developments, the market continues to focus on current fundamentals rather than unfolding geopolitical risks. Despite Iran’s recent attack on Israel, oil prices have slid, reflecting a sideways or slightly bearish sentiment. This morning, oil prices stand at USD 90 per barrel, down 2.5% from Friday’s highs.

The attack

Iran’s launch of over 300 rockets and drones toward Israel marks the first direct assault from Iranian territory since 1991. However, the attack, announced well in advance, resulted in minimal damage as Israeli and allied forces intercepted nearly all projectiles. Hence, the damage inflicted was limited. The incident has prompted US President Joe Biden to urge Israel to exercise restraint, as part of broader efforts to de-escalate tensions in the Middle East.

Israel’s response remains uncertain as its war cabinet deliberates on potential courses of action. While the necessity of a response is acknowledged, the timing and magnitude remain undecided.

The attack was allegedly in retaliation for an Israeli airstrike on Iran’s consulate in Damascus, resulting in significant casualties, including a senior leader in the Islamic Revolutionary Guard Corps’ elite Quds Force. It’s notable that this marks the first direct targeting of Israel from Iranian territory, setting the stage for heightened tensions between the two nations.

Despite the scale of the attack, the vast majority of Iranian projectiles were intercepted before reaching Israeli territory. However, a small number did land, causing minor damage to a military base in the southern region.

President Biden swiftly condemned Iran’s actions and pledged to coordinate a diplomatic response with leaders from the G7 nations. The US military’s rapid repositioning of assets in the region underscores the seriousness of the situation.

Iran’s willingness to escalate tensions further depends on Israel’s response, as indicated by General Mohammad Bagheri, chief of staff of the Iranian armed forces. Meanwhile, speculation about a retaliatory attack from Israel persists.

Looking ahead, key questions remain unanswered. Will Iran launch additional attacks? How will Israel respond, and what implications will it have for the region? Moreover, how will Iran’s allies react to the escalating tensions?

Given the potential for a full-scale war between Iran and Israel, concerns about its impact on global energy markets are growing. Both the United States and China have strong incentives to reduce tensions in the region, given the destabilizing effects of a regional conflict.

Our view in conclusion

The recent escalation between Iran and Israel underscores the delicate balance of power in the volatile Middle East. With tensions reaching unprecedented levels and the specter of further escalation looming, the potential for a full-blown conflict cannot be understated. The ramifications of such a scenario would be far-reaching and could have significant implications for regional stability and global security.

Turning to the oil market, there has been much speculation about the possibility of a full-scale blockade of the Strait of Hormuz in the event of further escalation. However, at present, such a scenario remains highly speculative. Nonetheless, it is crucial to note that Iran’s oil production and exports remain at risk even without further escalation. Currently producing close to 3.2 million barrels per day, Iran has significantly increased its production from mid-2020 levels of 1.9 million barrels per day.

In response to the recent attack, Israel may exert pressure on its ally, the US, to impose stricter sanctions on Iran. The enforcement of such sanctions, particularly on Iranian oil exports, could result in a loss of anywhere between 0.5 million to 1 million barrels per day of oil supply. This would likely keep the oil market in deficit for the remainder of the year, contradicting the Biden administration’s wish to maintain oil and gasoline prices at sustainable levels ahead of the election. While other OPEC nations have spare capacity, utilizing it would tighten the global oil market even further. Saudi Arabia and the UAE, for example, could collectively produce an additional almost 3 million barrels of oil per day if necessary.

Furthermore, both Iran and the US have expressed a desire to prevent further escalation. However, much depends on Israel’s response to the recent barrage of rockets. While Israel has historically refrained from responding violently to attacks (1991), the situation remains fluid. If Israel chooses not to respond forcefully, the US may be compelled to promise stronger enforcement of sanctions on Iranian oil exports. Consequently, Iranian oil exports are at risk, regardless of whether a wider confrontation ensues in the Middle East.

Analyzing the potential impact, approximately 2.2 million barrels per day of net Iranian crude and condensate exports could be at risk, factoring in Iranian domestic demand and condensate production. The effectiveness of US sanctions enforcement, however, remains uncertain, especially considering China’s stance on Iranian oil imports.

Despite these uncertainties, the market outlook remains cautiously optimistic for now, with Brent Crude expected to hover around the USD 90 per barrel mark in the near term. Navigating through geopolitical tensions and fundamental factors, the oil market continues to adapt to evolving conflicts in the Middle East and beyond.

Lots of talk about an increasingly tight oil market. And yes, the oil price will move higher as a result of this and most likely move towards USD 100/b. Tensions and flareups in the Middle East is little threat to oil supply and will be more like catalysts driving the oil price higher on the back of a fundamentally bullish market. I.e. flareups will be more like releasing factors. But OPEC+ will for sure produce more if needed as it has no interest in killing the goose (global economy) that lays the golden egg (oil demand growth). We’ll probably get verbal intervention by OPEC+ with ”.. more supply in H2” quite quickly when oil price moves closer to USD 100/b and that will likely subdue the bullishness. OPEC+ in full control of the oil market probably means an oil price ranging from USD 70/b to USD 100/b with an average of around USD 85/b. Just like last year.

Brent crude continues to trade around USD 90/b awaiting catalysts like further inventory declines or Mid East flareups. Brent crude ydy traded in a range of USD 88.78 – 91.1/b before settling at USD 90.38/b. Trading activity ydy seems like it was much about getting comfortable with 90-level. Is it too high? Is there still more upside etc. But in the end it settled above the 90-line. This morning it has traded consistently above the line without making any kind of great leap higher.

Netanyahu made it clear that Rafah will be attacked. Israel ydy pulled some troops out of Khan Younis in Gaza and that calmed nerves in the region a tiny bit. But it seems to be all about tactical preparations rather than an indication of a defuse of the situation. Ydy evening Benjamin Netanyahu in Israel made it clear that a date for an assault on Rafah indeed has been set despite Biden’s efforts to prevent him doing so. Article in FT on this today. So tension in Israel/Gaza looks set to rise in not too long. The market is also still awaiting Iran’s response to the bombing of its consulate in Damascus one week ago. There is of course no oil production in Israel/Gaza and not much in Syria, Lebanon or Yemen either. The effects on the oil market from tensions and flareups in these countries are first and foremost that they work as catalysts for the oil price to move higher in an oil market which is fundamentally bullish. Deficit and falling oil inventories is the fundamental reason for why the oil price is moving higher and for why it is at USD 90/b today. There is also the long connecting string of:

[Iran-Iraq-Syria/Yemen/Lebanon/Gaza – Israel – US]

which creates a remote risk that oil supply in the Middle East potentially could be at risk in the end when turmoil is flaring in the middle of this connecting string. This always creates discomfort in the oil market. But we see little risk premium for a scenario where oil supply is really hurt in the end as neither Iran nor the US wants to end up in such a situation.

Tight market but OPEC+ will for sure produce more if needed to prevent global economy getting hurt. There is increasing talk about the oil market getting very tight in H2-24 and that the oil price could shoot higher unless OPEC+ is producing more. But of course OPEC+ will indeed produce more. The health of the global economy is essential for OPEC+. Healthy oil demand growth is like the goose that lays the golden egg for them. In no way do they want to kill it with too high oil prices. Brent crude averaged USD 82.2/b last year with a high of USD 98/b. So far this year it has averaged USD 82.6/b. SEB’s forecast is USD 85/b for the average year with a high of USD 100/b. We think that a repetition of last year with respect to oil prices is great for OPEC+ and fully acceptable for the global economy and thus will not hinder a solid oil demand growth which OPEC+ needs. Nothing would make OPEC+ more happy than to produce at a normal level and still being able to get USD 85/b. Brent crude will head yet higher because OPEC+ continues to hold back supply Q2-24 resulting in declining inventories and thus higher prices. But when the oil price is nearing USD 100/b we expect verbal intervention from the group with statements like ”… more supply in H2-24” and that will probably dampen bullish prices.

Not only does OPEC+ want to produce at a normal level. It also needs to produce at a normal level. Because at some point in time in the future there will be a situation sooner or later where they will have to cut again. And unless they are back to normal production at that time they won’t be in a position to cut again.

So OPEC+ won’t kill the goose that lays the golden egg. They won’t allow the oil price to stay too high for too long. I.e. USD 100/b or higher. They will produce more in H2-24 if needed to prevent too high oil prices and they have the reserve capacity to do it.

Data today: US monthly oil market report (STEO) with forecast for US crude and liquids production at 18:00 CET

Brent crude is pulling back below the 90-line this morning trading as low as USD 88.78/b following a 4.2% gain last week. The pullback is blamed on news that Israel is pulling some troops out of Gaza. But we think this is much more of a technical move below the 90-line with preparations for further price gains ahead. The Israeli troop movements are a preparation for a final push into Rafah in Gaza to take out the last stronghold of Hamas there (FT article today). Iranian retaliation following the attack in Damascus last week also looks set to unfold in some way. Possibly by Hezbollah in Lebanon though instigated by Iran. Prepare for more turmoil, lower oil inventories and higher prices as the market continues to run a deficit.

Brent gained 4.2% last week with a solid close above the 90-line. Brent crude had a stellar week last week gaining 4.2%. Even following such a strong performance it made a gain on Friday of 0.6% with a close at USD 91.17/b. Friday also saw the highest trade of the week at USD 91.91/b.

Brent was propelled by positive PMI gains, geopolitics and falling US inventories. Oil was supported by a rang of factors last week. Both the US and China saw their manufacturing PMIs rise above the 50-line (50.3 and 50.8 resp.). The Eurozone manufacturing PMI rose to 46.1 from 45.7 while the composite index rose above the 50-line to 50.3 from 49.9. These PMI gains supported both oil and metals through growth recovery optimism. US oil inventories last Wednesday created less waves with a net draw of 2.2 m b in total crude and product inventories. It was still a very bullish reading in our view as inventories normally this time of year should have risen 3.8 m b. Thus driving US commercial oil inventories further away and below the normal level of inventories. Geopolitical focus flared up following the attack on Iran’s consulate in Syria where Iran’s top Islamic Revolutionary Guard Corps (IRGC) general in Syria along with five other IRGC officers were killed. Israel is assumed to be behind the attack but has not taken responsibility yet.

Back below 90 this morning in what seems like a geopolitical breather. But is more of a technical move. This morning Brent crude has pulled back and traded as low as USD 88.78/b while trading at USD 89.76/b. We commented on Friday that it is quite normal for Brent crude to pull back below big numbers after having broken them. Just to test out the level properly before heading higher.

Israel is pulling some troops out of Gaza. Most likely it is preparing to attack Rafah (FT today). Price action to the downside this morning is blamed on some kind of reduced geopolitical premium as Israel is withdrawing some of its troops in Gaza. The reason why it is withdrawing some tropes however is to our understanding that Israel is preparing to attack Rafah, the southernmost part of Gaza bordering to Egypt where now close to one million Palestinians are living. It is the last strong-hold of Hamas and Israel looks bent on taking it out despite repeated warnings against it from the US. Human tragedy looks set to unfold in Rafah in not too long.

”Iran will respond to the Damascus strike”. The most likely flareup is Lebanon and Hezbollah. The geopolitical flare following the attack on Iran’s consulate in Syria last week has faded a little this morning. But this is in no way over. John Sawers, former chief of MI6, in an article in FT on Friday bluntly stated: ”Iran will respond to the Damascus strike”. Iran still doesn’t want to be involved in direct military confrontation. The likely flareup will be Lebanon and Hezbollah which could force Israel into a two-front war.

Rafah is located in the southernmost part of Gaza

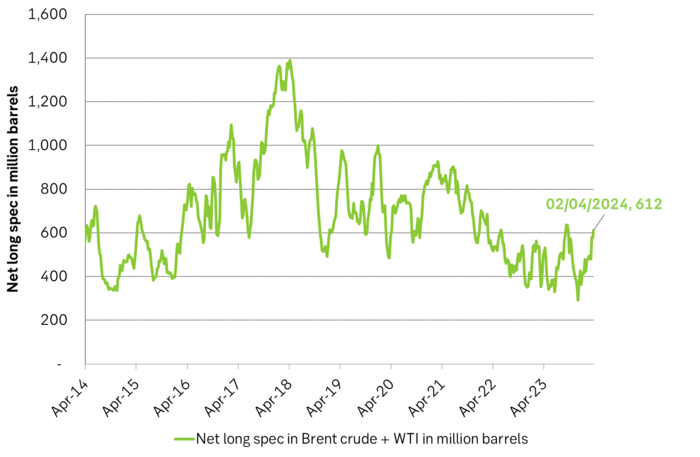

Net long specs in Brent + WTI rose by 34 m b over the week to 2 April.

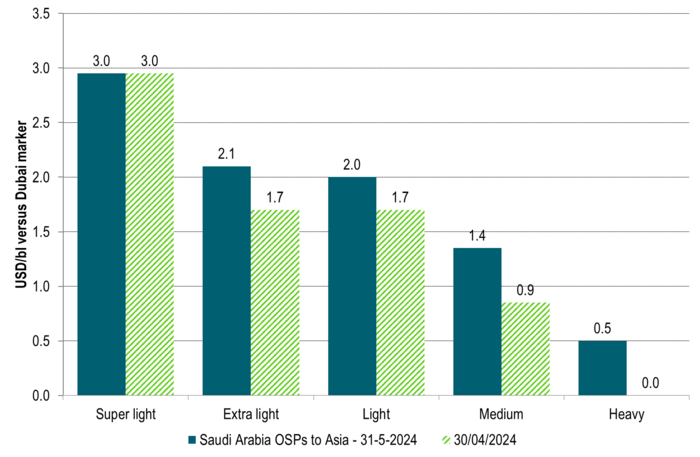

Saudi Arabia lifted its Official Selling Prices to Asia for most grades for May delivery

Mexikos sockerproduktion den lägsta på ett decennium

Kaffepriserna rör på sig

Brace for Covert Conflict

Ett atomlager guld – forskare på Linköpings universitet skapar guldén

Elpriset fortsätter att sjunka – halverade priser i april jämfört med 2023

Michel Rufli om trenderna som får guldpriset att stiga

Guld toppar 2200 USD per uns

Vertikal prisuppgång på kakao – priset toppar nu 9000 USD

Lundin Mining får köprekommendation av BMO

Guldpriset når nytt all time high och bryter igenom 2300 USD

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMichel Rufli om trenderna som får guldpriset att stiga

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanGuld toppar 2200 USD per uns

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVertikal prisuppgång på kakao – priset toppar nu 9000 USD

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanLundin Mining får köprekommendation av BMO

-

Nyheter2 veckor sedan

Guldpriset når nytt all time high och bryter igenom 2300 USD

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanCentralbanker fortsatte att köpa guld under februari

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanKaffepriserna stiger på lågt utbud och stark efterfrågan

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHur mår den svenska skogsbraschen? Två favoritaktier