Analys

SHB Råvarubrevet 17 maj 2013

Vårdepressionen mildras

Vårdepressionen mildras

Råvaror och räntemarknaden har till skillnad från börsen tagit till sig svagare makro under våren. Vår-depressionstemat fick sig dock en törn från den senaste amerikanska sysselsättningsstatistiken. Förutom en bättre utveckling än väntat i april reviderades historiken kraftigt i positiv riktning. Mycket talar nu för att årets vårdepression blir mildare än under tidigare år. Att börsen struntar helt och fullt i makrodata och fortsätter att stiga är ytterligare en faktor som talar för en mildare vårdepression. Om Fed lyckas elda på S&P500 med 5%+ per kvartal är det svårt att vara särskilt negativ på konsumtionstillväxten på kort sikt. Trots Fed:s aktioner så har inflationsförväntningarna åter börjat falla och det har dragit med sig guld brant nedåt efter rekylen på raset i april.

Marknaden är fortsatt väl understödda av centralbankers oro för nedsidesrisker. Den senaste tiden har centralbankerna i Australien, Danmark, EMU, Indien, Polen och Sydkorea sänkt räntorna. Federal Reserve påminde dessutom nyligen marknaderna att de inte bara kan minska tillgångsköpen, utan också öka dem om läget kräver det. Givet fortsatt svag tillväxt kommer exit från centralbanker långt ner på agendan och inget vi oroar oss för idag.

Basmetallerna

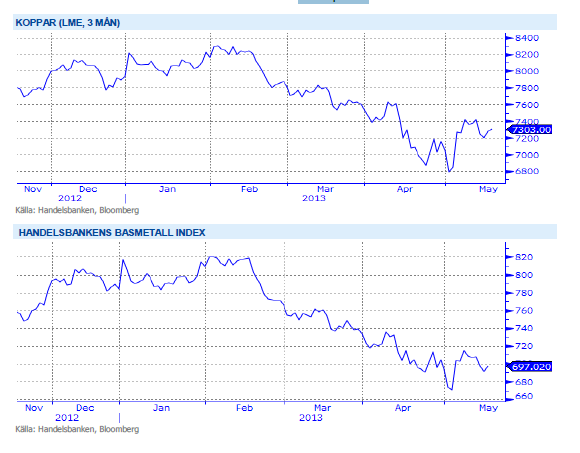

Kopparpriset får stöd

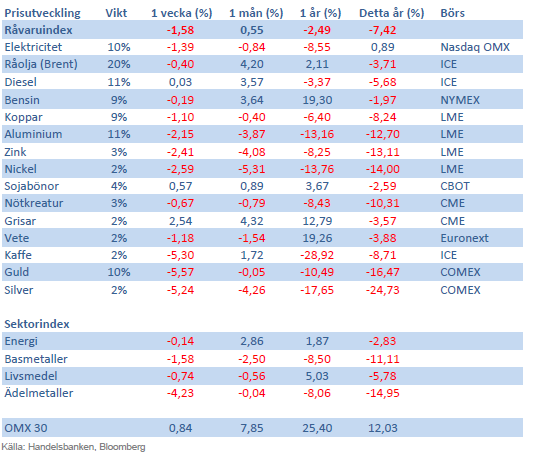

Basmetallerna fortsätter att handlas upp och ner främst på främst Kina och USA data. Förra veckan steg metallerna men har kommit ner efter Kinaoro denna vecka. Antal byggnadstillstånd i USA kom in bättre än väntat för april månad och ligger nu på fem årshögsta, vilket ger stöd till bl.a. kopparpriset då nya hus kräver mycket koppar. Kopparn stärktes även under veckan efter Shanghailager visar lägsta lager på 8 månader.

Vid Freeport-McMoRan koppargruva (världens nästa största) i Sydafrika rasade en tunnel in i tisdags där hittills 5 personer har omkommit. Räddningsarbetet fortsätter där man nu hittat 10 överlevande, men fortfarande saknas 23 arbetare som antas vara instängda. Arbetet har stannat upp något men tros inte ha något tydlig inverkan på produktionen.

Vi tror fortsatt att basmetallerna kan försvagas om makrodata inte förbättras, men ser dagens nivåer som köpvärda.

Trots fortsatt svag makromiljö och fortsatt risk på nedsidan ser vi ändå basmetaller som köpvärda på dessa nivåer. Vi tror på: LONG BASMET H

Ädelmetaller

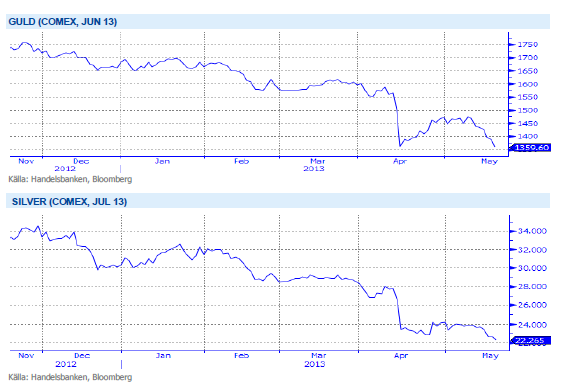

Guldet fortfarande dyrt

Guldet har återigen börjat falla, helt i linje med vår tro. Kollapsen i april, då guldet föll med 15 % på två dagar, har åtföljts av en rekyl från 1 350 dollar per uns upp till nästan 1 480 dollar. Vi har hela tiden sagt att detta inte är ett köpläge, utan att guldets resa kommer att vara fortsatt nedåt. Detta gäller fortfarande, vi ser på prisuppgångar som bra tillfällen att sälja av långa positioner, eller till att gå kort den ädla metallen. Den senaste veckan har guldet tappat drygt 5 %, och handlar nu på 1 370 dollar, eller bara 20 dollar över botten från april-raset. Alla som tagit tillfället i akt att ”köpa billigt” – vilket väldigt många gjort – kommer att behöva testa sin övertygelse om vi skulle gå under 1 350 igen. Silvret – guldets stökige lillebror – förnekar sig inte och handlas redan nu till lägre priser än sin botten från april.

Resonemanget är detsamma nu som tidigare, att guldet köper man bara för att tjäna pengar, man köper det inte för att använda det till något vettigt. Priset sätts helt i investerarmarknaden, smyckes- och industridelen är förvisso inte betydelselösa för den årliga nyproduktionen av guld, men det är inte i dessa delar som priset sätts. Kom ihåg att allt guld som någonsin producerats fortfarande finns, det ligger och samlar damm och bevakas till höga kostnader, allt för att det ska bevara värdet…

Och när folk säljer guld på riktigt, då blir det trångt i dörren. Guldet är fortfarande väldigt dyrt.

Trots det största raset på 30 år tror vi att förtroendet för guld håller på urholkas och att trenden nedåt fortsätter. Vi tror på: SHRT GULD H

Energi

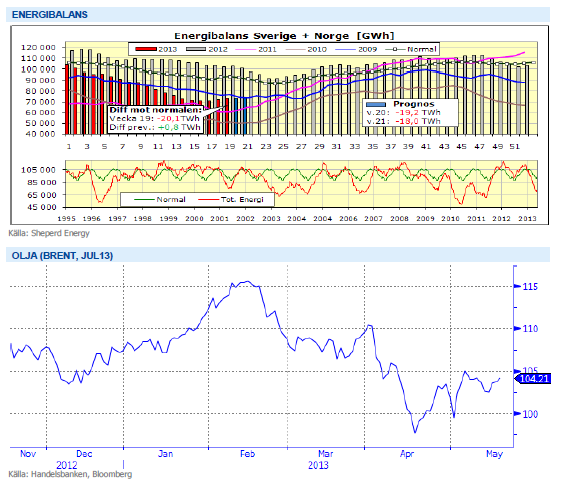

Förbättrad energibalans!

Elkontraktet Q3 2013 handlas ner mot 40 euro och marknaden har nu justerat för de svaga signaler vi haft de senaste två veckorna. Såväl energikol som utsläppsrätter och pris på kontinentala elmarknader har bidragit till nedgången och vi räknar nu med att marknaden stabiliseras kring denna nivå med stöd från rådande underskott i energibalansen (-20 TWh se nedan) och förhållandevis höga spotprisnivåer. Utsläppsrätterna kvar i en tradingrange på 3-4 euro vilket lär bestå tills vi får någon form av signal eller nytt förslag till att minska överskottet. Senaste nederbördsprognosen för de kommande 10 dagarna visar ett överskott om ca 2 TWh.

Oljan (brent) har handlats upp under veckan och handlas nu på 104 USD/fat vilket är 1,2 % högre än månagens öppning. Positiva signaler från Fed ger stöd men även ökad bilförsäljning i Europa. Enligt ACEA (Automobile Manufacturers Association) stiger bilförsäljningen i Tyskland och Spanien vilket ökar efterfrågan på bensin.

Livsmedel

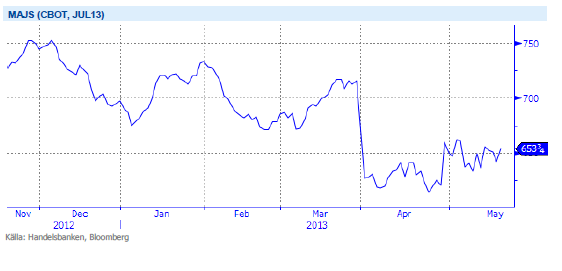

Det finns hopp för majsen

Priset på majs i Chicago har gått ned något under veckan, det delvis som följd av hopp om bättre väder och en högre takt på sådden i USA. Veckan som gått har inte varit optimal med fortsatt fördröjande regnskurar i en del områden, vilka visserligen gynnar redan sådd gröda. För tillfället är avklarad sådd vid denna tid på året den lägsta sedan 1980, dock finns alltså hopp om förbättring framöver. År med sen sådd har tidigare kunnat ge en hög avkastning, varför vi ännu inte finner skäl att tro på annat än klart högre produktion än förra året – med lägre priser som följd.

Priserna på sojabönor i Chicago har gått upp sedan förra veckan. Stöd till priserna kommer delvis från små lager av gammal skörd i kombination med fortsatt hyfsad exporttakt, inte minst för sojamjöl. Sen sådd i USA även för sojabönorna ger även det stöd till priserna. Nu gällande väderprognoser ser ut att bjuda på klart bättre väder i nästa vecka, vilket bör snabba på sådden. Sojabönornas odlingssäsong är senare än majsens och än finns inga större skäl till oro för den amerikanska sojan, gott om tid finns att få sådden klar inom rimlig tid. I dagsläget finns inga skäl till att inte tro på ökad produktion dels i viktiga USA men även i andra delar av världen – vilket talar för lägre priser längre fram på året

Vi behåller dock neutral vy för sektorn livsmedel på kort sikt då viss risk kvarstår.

Då priserna har på de stora jordbruksråvarorna soja, majs och vete har fallit tillbaka till nivåer före torkan i USA, tror vi att en nedsida är begränsad på kort sikt och därför är vi neutrala till utvecklingen för denna sektor.

Handelsbankens Råvaruindex

Handelsbankens råvaruindex består av de underliggande indexen för respektive råvara. Vikterna är bestämda till hälften från värdet av nordisk produktion (globala produktionen för sektorindex) och till hälften från likviditeten i terminskontrakten.

[box]SHB Råvarubrevet är producerat av Handelsbanken och publiceras i samarbete och med tillstånd på Råvarumarknaden.se[/box]

Ansvarsbegränsning

Detta material är producerat av Svenska Handelsbanken AB (publ) i fortsättningen kallad Handelsbanken. De som arbetar med innehållet är inte analytiker och materialet är inte oberoende investeringsanalys. Innehållet är uteslutande avsett för kunder i Sverige. Syftet är att ge en allmän information till Handelsbankens kunder och utgör inte ett personligt investeringsråd eller en personlig rekommendation. Informationen ska inte ensamt utgöra underlag för investeringsbeslut. Kunder bör inhämta råd från sina rådgivare och basera sina investeringsbeslut utifrån egen erfarenhet.

Informationen i materialet kan ändras och också avvika från de åsikter som uttrycks i oberoende investeringsanalyser från Handelsbanken. Informationen grundar sig på allmänt tillgänglig information och är hämtad från källor som bedöms som tillförlitliga, men riktigheten kan inte garanteras och informationen kan vara ofullständig eller nedkortad. Ingen del av förslaget får reproduceras eller distribueras till någon annan person utan att Handelsbanken dessförinnan lämnat sitt skriftliga medgivande. Handelsbanken ansvarar inte för att materialet används på ett sätt som strider mot förbudet mot vidarebefordran eller offentliggörs i strid med bankens regler.

Brent crude spikes to USD 90.75/b before falling back as Iran plays it down. Brent crude fell sharply on Wednesday following fairly bearish US oil inventory data and yesterday it fell all the way to USD 86.09/b before a close of USD 87.11/b. Quite close to where Brent traded before the 1 April attack. This morning Brent spiked back up to USD 90.75/b (+4%) on news of Israeli retaliatory attack on Iran. Since then it has quickly fallen back to USD 88.2/b, up only 1.3% vs. ydy close.

The fear is that we are on an escalating tit-for-tat retaliatory path. Following explosions in Iran this morning the immediate fear was that we now are on a tit-for-tat escalating retaliatory path which in the could end up in an uncontrollable war where the US unwillingly is pulled into an armed conflict with Iran. Iran has however largely diffused this fear as it has played down the whole thing thus signalling that the risk for yet another leg higher in retaliatory strikes from Iran towards Israel appears low.

The hope is that the retaliatory strikes will be fading in magnitude and then fizzle out. What we can hope for is that the current tit-for-tat retaliatory strikes are fading in magnitude rather than rising in magnitude. Yes, Iran may retaliate to what Israel did this morning, but the hope if it does is that it is of fading magnitude rather than escalating magnitude.

Israel is playing with ”US house money”. What is very clear is that neither the US nor Iran want to end up in an armed conflict with each other. The US concern is that it involuntary is dragged backwards into such a conflict if Israel cannot control itself. As one US official put it: ”Israel is playing with (US) house money”. One can only imagine how US diplomatic phone lines currently are running red-hot with frenetic diplomatic efforts to try to defuse the situation.

It will likely go well as neither the US nor Iran wants to end up in a military conflict with each other. The underlying position is that both the US and Iran seems to detest the though of getting involved in a direct military conflict with each other and that the US is doing its utmost to hold back Israel. This is probably going a long way to convince the market that this situation is not going to fully blow up.

The oil market is nonetheless concerned as there is too much oil supply at stake. The oil market is however still naturally concerned and uncomfortable about the whole situation as there is so much oil supply at stake if the situation actually did blow up. Reports of traders buying far out of the money call options is a witness of that.

Throughout this week, the Brent Crude price has experienced a decline of USD 3 per barrel, despite ongoing turmoil in the Middle East. Price fluctuations have ranged from highs of USD 91 per barrel at the beginning of the week to lows of USD 87 per barrel as of yesterday evening.

Following the release of yesterday’s US inventory report, Brent Crude once again demonstrated resilience against broader macroeconomic concerns, instead focusing on underlying market fundamentals.

Nevertheless, the recent drop in prices may come as somewhat surprising given the array of conflicting signals observed. Despite an increase in US inventories—a typically bearish indicator—we’ve also witnessed escalating tensions in the Middle East, coupled with the reinstatement of US sanctions on Venezuela. Furthermore, there are indications of impending sanctions on Iran in response to the recent attack on Israel.

Treasury Secretary Janet Yellen has indicated that new sanctions targeting Iran, particularly aimed at restricting its oil exports, could be announced as early as this week. As previously highlighted, we maintain the view that Iran’s oil exports remain vulnerable even without further escalation of the conflict. It appears that Israel is exerting pressure on its ally, the US, to impose stricter sanctions on Iran, an action that is unfolding before our eyes.

Iran’s current oil production stands at close to 3.2 million barrels per day. Considering additional condensate production of about 0.8 million barrels per day and subtracting domestic demand of roughly 1.8 million barrels per day, the net export of Iranian crude and condensate is approximately 2.2 million barrels per day.

However, the uncertainty surrounding the enforcement of such sanctions casts doubt on the likelihood of a complete ending of Iranian exports. Approximately 80% of Iran’s exports are directed to independent refineries in China, suggesting that US sanctions may have limited efficacy unless China complies. The prospect of China resisting US pressure on its oil imports from Iran poses a significant challenge to US sanctions enforcement efforts.

Furthermore, any shortfall resulting from sanctions could potentially be offset by other OPEC nations with spare capacity. Saudi Arabia and the UAE, for instance, can collectively produce an additional almost 3 million barrels of oil per day, although this remains a contingency measure.

In addition to developments related to Iran, the Biden administration has re-imposed restrictions on Venezuelan oil, marking the end of a six-month reprieve. This move is expected to impact flows from the South American nation.

Meanwhile, US crude inventories (excluding SPR holdings) surged by 2.7 million barrels last week (page 11 attached), reaching their highest level since June of last year. This increase coincided with a decline in measures of fuel demand (page 14 attached), underscoring a slightly weaker US market.

In summary, while geopolitical tensions persist and new rounds of sanctions are imposed, our market outlook remains intact. We maintain our forecast of an average Brent Crude price of USD 85 per barrel for the year 2024. In the short term, however, prices are expected to hover around the USD 90 per barrel mark as they navigate through geopolitical uncertainties and fundamental factors.

In the past two trading days, Brent Crude prices have fluctuated between highs of USD 92.2 per barrel and lows of USD 88.7 per barrel. Despite escalation tensions in the Middle East, oil prices have remained relatively stable over the past 24 hours. The recent barrage of rockets and drones in the region hasn’t significantly affected market sentiment regarding potential disruptions to oil supply. The key concern now is how Israel will respond: will it choose a strong retaliation to assert deterrence, risking wider regional instability, or will it revert to targeted strikes on Iran’s proxies in Lebanon, Syria, Yemen, and Iraq? While it’s too early to predict, one thing is clear: brace for increased volatility, uncertainty, and speculation.

Amidst these developments, the market continues to focus on current fundamentals rather than unfolding geopolitical risks. Despite Iran’s recent attack on Israel, oil prices have slid, reflecting a sideways or slightly bearish sentiment. This morning, oil prices stand at USD 90 per barrel, down 2.5% from Friday’s highs.

The attack

Iran’s launch of over 300 rockets and drones toward Israel marks the first direct assault from Iranian territory since 1991. However, the attack, announced well in advance, resulted in minimal damage as Israeli and allied forces intercepted nearly all projectiles. Hence, the damage inflicted was limited. The incident has prompted US President Joe Biden to urge Israel to exercise restraint, as part of broader efforts to de-escalate tensions in the Middle East.

Israel’s response remains uncertain as its war cabinet deliberates on potential courses of action. While the necessity of a response is acknowledged, the timing and magnitude remain undecided.

The attack was allegedly in retaliation for an Israeli airstrike on Iran’s consulate in Damascus, resulting in significant casualties, including a senior leader in the Islamic Revolutionary Guard Corps’ elite Quds Force. It’s notable that this marks the first direct targeting of Israel from Iranian territory, setting the stage for heightened tensions between the two nations.

Despite the scale of the attack, the vast majority of Iranian projectiles were intercepted before reaching Israeli territory. However, a small number did land, causing minor damage to a military base in the southern region.

President Biden swiftly condemned Iran’s actions and pledged to coordinate a diplomatic response with leaders from the G7 nations. The US military’s rapid repositioning of assets in the region underscores the seriousness of the situation.

Iran’s willingness to escalate tensions further depends on Israel’s response, as indicated by General Mohammad Bagheri, chief of staff of the Iranian armed forces. Meanwhile, speculation about a retaliatory attack from Israel persists.

Looking ahead, key questions remain unanswered. Will Iran launch additional attacks? How will Israel respond, and what implications will it have for the region? Moreover, how will Iran’s allies react to the escalating tensions?

Given the potential for a full-scale war between Iran and Israel, concerns about its impact on global energy markets are growing. Both the United States and China have strong incentives to reduce tensions in the region, given the destabilizing effects of a regional conflict.

Our view in conclusion

The recent escalation between Iran and Israel underscores the delicate balance of power in the volatile Middle East. With tensions reaching unprecedented levels and the specter of further escalation looming, the potential for a full-blown conflict cannot be understated. The ramifications of such a scenario would be far-reaching and could have significant implications for regional stability and global security.

Turning to the oil market, there has been much speculation about the possibility of a full-scale blockade of the Strait of Hormuz in the event of further escalation. However, at present, such a scenario remains highly speculative. Nonetheless, it is crucial to note that Iran’s oil production and exports remain at risk even without further escalation. Currently producing close to 3.2 million barrels per day, Iran has significantly increased its production from mid-2020 levels of 1.9 million barrels per day.

In response to the recent attack, Israel may exert pressure on its ally, the US, to impose stricter sanctions on Iran. The enforcement of such sanctions, particularly on Iranian oil exports, could result in a loss of anywhere between 0.5 million to 1 million barrels per day of oil supply. This would likely keep the oil market in deficit for the remainder of the year, contradicting the Biden administration’s wish to maintain oil and gasoline prices at sustainable levels ahead of the election. While other OPEC nations have spare capacity, utilizing it would tighten the global oil market even further. Saudi Arabia and the UAE, for example, could collectively produce an additional almost 3 million barrels of oil per day if necessary.

Furthermore, both Iran and the US have expressed a desire to prevent further escalation. However, much depends on Israel’s response to the recent barrage of rockets. While Israel has historically refrained from responding violently to attacks (1991), the situation remains fluid. If Israel chooses not to respond forcefully, the US may be compelled to promise stronger enforcement of sanctions on Iranian oil exports. Consequently, Iranian oil exports are at risk, regardless of whether a wider confrontation ensues in the Middle East.

Analyzing the potential impact, approximately 2.2 million barrels per day of net Iranian crude and condensate exports could be at risk, factoring in Iranian domestic demand and condensate production. The effectiveness of US sanctions enforcement, however, remains uncertain, especially considering China’s stance on Iranian oil imports.

Despite these uncertainties, the market outlook remains cautiously optimistic for now, with Brent Crude expected to hover around the USD 90 per barrel mark in the near term. Navigating through geopolitical tensions and fundamental factors, the oil market continues to adapt to evolving conflicts in the Middle East and beyond.

AI ökar det totala elbehovet i USA med 100 % kommande 15 år

Fear that retaliations will escalate but hopes that they are fading in magnitude

Fundamentals trump geopolitical tensions

Fortum och Vargön Alloys tecknar femårigt avtal om kärnkraftsel

Kärnkraftreaktorutvecklaren Blykalla har gjort en kapitalanskaffning på 80 Mkr

Guldpriset når nytt all time high och bryter igenom 2300 USD

Guld toppar 2200 USD per uns

Lundin Mining får köprekommendation av BMO

Vertikal prisuppgång på kakao – priset toppar nu 9000 USD

Kaffepriserna stiger på lågt utbud och stark efterfrågan

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanGuldpriset når nytt all time high och bryter igenom 2300 USD

-

Nyheter4 veckor sedan

Guld toppar 2200 USD per uns

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanLundin Mining får köprekommendation av BMO

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanVertikal prisuppgång på kakao – priset toppar nu 9000 USD

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanKaffepriserna stiger på lågt utbud och stark efterfrågan

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanCentralbanker fortsatte att köpa guld under februari

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHur mår den svenska skogsbraschen? Två favoritaktier

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanKakaomarknaden är extrem för tillfället

Bonden

17 maj, 2013 vid 23:50

Inga kommentarer kring WASDE-rapporten som kom förra veckan. Hade varit intressant att se vad Handelsbanken hade för åsikt om det stor fallet i spannmål som kom direkt efter den.