Analys

Searching for the US shale oil price floor

In hindsight the market was obviously not satisfied with OPEC just rolling their cuts over for another 9 months. The market’ judgement was clearly that that was far from enough. So if OPEC & Co’s production cuts were judged to be insufficient to balance the market then the price itself will have to do the job or a part of the job as well. If so, then the question is at what level do the oil price need to move to in order to shift US shale oil rig count from expansion to neutral or contraction.

In hindsight the market was obviously not satisfied with OPEC just rolling their cuts over for another 9 months. The market’ judgement was clearly that that was far from enough. So if OPEC & Co’s production cuts were judged to be insufficient to balance the market then the price itself will have to do the job or a part of the job as well. If so, then the question is at what level do the oil price need to move to in order to shift US shale oil rig count from expansion to neutral or contraction.

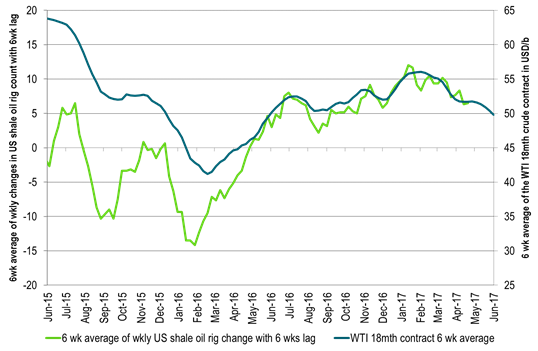

The US shale oil space has now been in one loooong expansion phase continuously for one year. First in terms of rig additions). So our current empirical knowledge is actually one year old from when we experienced that US shale oil rig count started to expand when the US WTI 18 mth contract crossed above $46-47/b however with a 6 weeks lag. Has this inflection point shifted higher or lower over the last year? The market doesn’t really know and now it needs to know. Shale oil productivity and technology improvements and further spreading of “best practice” from the leading companies to the less advanced has probably shifted it lower. Cost inflation is however clearly evident and is working in the other direction. Fracking and completion of wells seems to be a bottleneck at the moment. This should make companies more caution in terms of adding more drilling rigs. No point in more rigs and more wells if you cannot complete them and move them into production.

The one and a half year forward WTI crude oil price (18thm contract) yesterday briefly traded down to $47.2/b before closing the day at $47.89/b. Thus right down to the empirical “shale oil floor” before bouncing up again. The 30 day average (6 weeks) for this contract is today $49.5/b. Thus we are at least starting to get close to the empirical inflection point from last year. We should thus soon see much softer growth in the US shale oil rig count and then it eventually should crawl to a halt if the WTI 18 mth contract continues to trade at current level of $47.5/b. Unless of course the inflection point has shifted yet lower today than where it was last year. This is clearly possible and it is also clearly what the market needs to know.

The US EIA this week released its monthly energy report. Its prognosis was that there was no deficit on the horizon for the global oil market within their outlook to 2018. Actually they project that the OECD stocks inches slightly higher y/y to end 2017 and then again a little higher y/y to end 2018. That was depressing for the bulls and it again strengthened the post OPEC view that what OPEC has decided to do is not going to be enough. The EIA actually agrees with this view.

Then on Wednesday, just one day after the EIA’s monthly report, data was released showing a big jump in oil inventories with crude stocks up 3.3 mb, gasoline up 3.3 mb and distillates up 4.4 mb with total for the three up 11 mb. That was kind of a nail in the coffin for the oil bulls and the oil price sold off sharply.

The whole debacle around Qatar has not been good for the oil price either with concerns that increasing disagreement between the OPEC countries could possibly undermine the current agreement for production cuts. Historically however OPEC has managed to sail through major political differences while still maintaining production cuts or strategies.

The price declines over the last week has primarily taken place at the front end of the forward curve where the front end has dipped 5.5% while the longer dated Brent December 2020 contract has only declined 0.5%. So no major sell-off along the curve. The sell-off in the front end of the curve is a signal of concerns for high inventories which won’t go away.

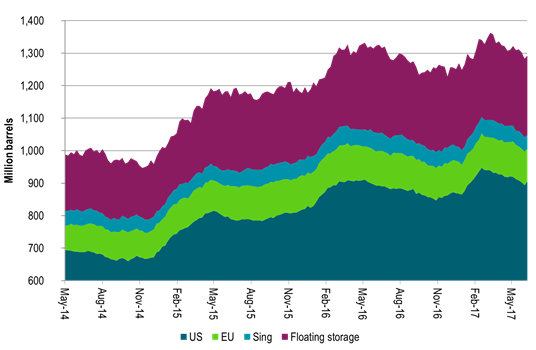

We do agree that it would be a good thing to get a refresh of where the current US shale oil rig inflection point is today as it is a full year since last time. However, we do disagree with the current view that OPEC & Co’s cuts won’t do the trick in 2017. We still strongly believe (baring Nigeria and Libya revival) that OECD’s commercial inventories will draw down strongly through H2-17 and stand close to normal by the end of the year in strong contrast to the latest monthly report from the US EIA. The inventories in weekly data have drawn down strongly since mid-March. Yes, this week they went up by some 10 mb for US, EU, Sing and floating combined, but last week it went down by 20 mb. In total they have drawn down 70 mb since mid-March and more is to come as we head into H2-17 with strong revival in global refining activity. We thus expect that the current view that there will be no draws in OECD stocks in 2017 displayed by the EIA this week will evaporate in not too long. We also think that OPEC’s production cuts will not fall apart due to the current debacle surrounding Qatar.

As such we don’t expect the current depression in oil prices to last through to the end of the year. We may have to hold out for a little while in order to figure out where the current US shale oil rig count inflection point is – where “the US shale oil price floor” currently is, but continued solid inventory draws should soon convince the market again that the market is surly running a deficit.

Today at 19.00 CET we have the Baker Hughes US rig count. Highly interesting to see whether the last six weeks with an average WTI 18 mth price of $49.5/b has started to slow down the US shale oil rig count growth.

Ch1 – Where is the “US shale oil price floor”? Still at $46-47/b (WTI 18 mth reference)?

Ch2: US inventories did counter the downward trend this week. But that should be noise

We still expect inventories to draw down across the board the coming half year

Kind regards

Bjarne Schieldrop

Chief analyst, Commodities

SEB Markets

Merchant Banking

Brent crude spikes to USD 90.75/b before falling back as Iran plays it down. Brent crude fell sharply on Wednesday following fairly bearish US oil inventory data and yesterday it fell all the way to USD 86.09/b before a close of USD 87.11/b. Quite close to where Brent traded before the 1 April attack. This morning Brent spiked back up to USD 90.75/b (+4%) on news of Israeli retaliatory attack on Iran. Since then it has quickly fallen back to USD 88.2/b, up only 1.3% vs. ydy close.

The fear is that we are on an escalating tit-for-tat retaliatory path. Following explosions in Iran this morning the immediate fear was that we now are on a tit-for-tat escalating retaliatory path which in the could end up in an uncontrollable war where the US unwillingly is pulled into an armed conflict with Iran. Iran has however largely diffused this fear as it has played down the whole thing thus signalling that the risk for yet another leg higher in retaliatory strikes from Iran towards Israel appears low.

The hope is that the retaliatory strikes will be fading in magnitude and then fizzle out. What we can hope for is that the current tit-for-tat retaliatory strikes are fading in magnitude rather than rising in magnitude. Yes, Iran may retaliate to what Israel did this morning, but the hope if it does is that it is of fading magnitude rather than escalating magnitude.

Israel is playing with ”US house money”. What is very clear is that neither the US nor Iran want to end up in an armed conflict with each other. The US concern is that it involuntary is dragged backwards into such a conflict if Israel cannot control itself. As one US official put it: ”Israel is playing with (US) house money”. One can only imagine how US diplomatic phone lines currently are running red-hot with frenetic diplomatic efforts to try to defuse the situation.

It will likely go well as neither the US nor Iran wants to end up in a military conflict with each other. The underlying position is that both the US and Iran seems to detest the though of getting involved in a direct military conflict with each other and that the US is doing its utmost to hold back Israel. This is probably going a long way to convince the market that this situation is not going to fully blow up.

The oil market is nonetheless concerned as there is too much oil supply at stake. The oil market is however still naturally concerned and uncomfortable about the whole situation as there is so much oil supply at stake if the situation actually did blow up. Reports of traders buying far out of the money call options is a witness of that.

Throughout this week, the Brent Crude price has experienced a decline of USD 3 per barrel, despite ongoing turmoil in the Middle East. Price fluctuations have ranged from highs of USD 91 per barrel at the beginning of the week to lows of USD 87 per barrel as of yesterday evening.

Following the release of yesterday’s US inventory report, Brent Crude once again demonstrated resilience against broader macroeconomic concerns, instead focusing on underlying market fundamentals.

Nevertheless, the recent drop in prices may come as somewhat surprising given the array of conflicting signals observed. Despite an increase in US inventories—a typically bearish indicator—we’ve also witnessed escalating tensions in the Middle East, coupled with the reinstatement of US sanctions on Venezuela. Furthermore, there are indications of impending sanctions on Iran in response to the recent attack on Israel.

Treasury Secretary Janet Yellen has indicated that new sanctions targeting Iran, particularly aimed at restricting its oil exports, could be announced as early as this week. As previously highlighted, we maintain the view that Iran’s oil exports remain vulnerable even without further escalation of the conflict. It appears that Israel is exerting pressure on its ally, the US, to impose stricter sanctions on Iran, an action that is unfolding before our eyes.

Iran’s current oil production stands at close to 3.2 million barrels per day. Considering additional condensate production of about 0.8 million barrels per day and subtracting domestic demand of roughly 1.8 million barrels per day, the net export of Iranian crude and condensate is approximately 2.2 million barrels per day.

However, the uncertainty surrounding the enforcement of such sanctions casts doubt on the likelihood of a complete ending of Iranian exports. Approximately 80% of Iran’s exports are directed to independent refineries in China, suggesting that US sanctions may have limited efficacy unless China complies. The prospect of China resisting US pressure on its oil imports from Iran poses a significant challenge to US sanctions enforcement efforts.

Furthermore, any shortfall resulting from sanctions could potentially be offset by other OPEC nations with spare capacity. Saudi Arabia and the UAE, for instance, can collectively produce an additional almost 3 million barrels of oil per day, although this remains a contingency measure.

In addition to developments related to Iran, the Biden administration has re-imposed restrictions on Venezuelan oil, marking the end of a six-month reprieve. This move is expected to impact flows from the South American nation.

Meanwhile, US crude inventories (excluding SPR holdings) surged by 2.7 million barrels last week (page 11 attached), reaching their highest level since June of last year. This increase coincided with a decline in measures of fuel demand (page 14 attached), underscoring a slightly weaker US market.

In summary, while geopolitical tensions persist and new rounds of sanctions are imposed, our market outlook remains intact. We maintain our forecast of an average Brent Crude price of USD 85 per barrel for the year 2024. In the short term, however, prices are expected to hover around the USD 90 per barrel mark as they navigate through geopolitical uncertainties and fundamental factors.

In the past two trading days, Brent Crude prices have fluctuated between highs of USD 92.2 per barrel and lows of USD 88.7 per barrel. Despite escalation tensions in the Middle East, oil prices have remained relatively stable over the past 24 hours. The recent barrage of rockets and drones in the region hasn’t significantly affected market sentiment regarding potential disruptions to oil supply. The key concern now is how Israel will respond: will it choose a strong retaliation to assert deterrence, risking wider regional instability, or will it revert to targeted strikes on Iran’s proxies in Lebanon, Syria, Yemen, and Iraq? While it’s too early to predict, one thing is clear: brace for increased volatility, uncertainty, and speculation.

Amidst these developments, the market continues to focus on current fundamentals rather than unfolding geopolitical risks. Despite Iran’s recent attack on Israel, oil prices have slid, reflecting a sideways or slightly bearish sentiment. This morning, oil prices stand at USD 90 per barrel, down 2.5% from Friday’s highs.

The attack

Iran’s launch of over 300 rockets and drones toward Israel marks the first direct assault from Iranian territory since 1991. However, the attack, announced well in advance, resulted in minimal damage as Israeli and allied forces intercepted nearly all projectiles. Hence, the damage inflicted was limited. The incident has prompted US President Joe Biden to urge Israel to exercise restraint, as part of broader efforts to de-escalate tensions in the Middle East.

Israel’s response remains uncertain as its war cabinet deliberates on potential courses of action. While the necessity of a response is acknowledged, the timing and magnitude remain undecided.

The attack was allegedly in retaliation for an Israeli airstrike on Iran’s consulate in Damascus, resulting in significant casualties, including a senior leader in the Islamic Revolutionary Guard Corps’ elite Quds Force. It’s notable that this marks the first direct targeting of Israel from Iranian territory, setting the stage for heightened tensions between the two nations.

Despite the scale of the attack, the vast majority of Iranian projectiles were intercepted before reaching Israeli territory. However, a small number did land, causing minor damage to a military base in the southern region.

President Biden swiftly condemned Iran’s actions and pledged to coordinate a diplomatic response with leaders from the G7 nations. The US military’s rapid repositioning of assets in the region underscores the seriousness of the situation.

Iran’s willingness to escalate tensions further depends on Israel’s response, as indicated by General Mohammad Bagheri, chief of staff of the Iranian armed forces. Meanwhile, speculation about a retaliatory attack from Israel persists.

Looking ahead, key questions remain unanswered. Will Iran launch additional attacks? How will Israel respond, and what implications will it have for the region? Moreover, how will Iran’s allies react to the escalating tensions?

Given the potential for a full-scale war between Iran and Israel, concerns about its impact on global energy markets are growing. Both the United States and China have strong incentives to reduce tensions in the region, given the destabilizing effects of a regional conflict.

Our view in conclusion

The recent escalation between Iran and Israel underscores the delicate balance of power in the volatile Middle East. With tensions reaching unprecedented levels and the specter of further escalation looming, the potential for a full-blown conflict cannot be understated. The ramifications of such a scenario would be far-reaching and could have significant implications for regional stability and global security.

Turning to the oil market, there has been much speculation about the possibility of a full-scale blockade of the Strait of Hormuz in the event of further escalation. However, at present, such a scenario remains highly speculative. Nonetheless, it is crucial to note that Iran’s oil production and exports remain at risk even without further escalation. Currently producing close to 3.2 million barrels per day, Iran has significantly increased its production from mid-2020 levels of 1.9 million barrels per day.

In response to the recent attack, Israel may exert pressure on its ally, the US, to impose stricter sanctions on Iran. The enforcement of such sanctions, particularly on Iranian oil exports, could result in a loss of anywhere between 0.5 million to 1 million barrels per day of oil supply. This would likely keep the oil market in deficit for the remainder of the year, contradicting the Biden administration’s wish to maintain oil and gasoline prices at sustainable levels ahead of the election. While other OPEC nations have spare capacity, utilizing it would tighten the global oil market even further. Saudi Arabia and the UAE, for example, could collectively produce an additional almost 3 million barrels of oil per day if necessary.

Furthermore, both Iran and the US have expressed a desire to prevent further escalation. However, much depends on Israel’s response to the recent barrage of rockets. While Israel has historically refrained from responding violently to attacks (1991), the situation remains fluid. If Israel chooses not to respond forcefully, the US may be compelled to promise stronger enforcement of sanctions on Iranian oil exports. Consequently, Iranian oil exports are at risk, regardless of whether a wider confrontation ensues in the Middle East.

Analyzing the potential impact, approximately 2.2 million barrels per day of net Iranian crude and condensate exports could be at risk, factoring in Iranian domestic demand and condensate production. The effectiveness of US sanctions enforcement, however, remains uncertain, especially considering China’s stance on Iranian oil imports.

Despite these uncertainties, the market outlook remains cautiously optimistic for now, with Brent Crude expected to hover around the USD 90 per barrel mark in the near term. Navigating through geopolitical tensions and fundamental factors, the oil market continues to adapt to evolving conflicts in the Middle East and beyond.

AI ökar det totala elbehovet i USA med 100 % kommande 15 år

Fear that retaliations will escalate but hopes that they are fading in magnitude

Fundamentals trump geopolitical tensions

Fortum och Vargön Alloys tecknar femårigt avtal om kärnkraftsel

Kärnkraftreaktorutvecklaren Blykalla har gjort en kapitalanskaffning på 80 Mkr

Guldpriset når nytt all time high och bryter igenom 2300 USD

Guld toppar 2200 USD per uns

Lundin Mining får köprekommendation av BMO

Vertikal prisuppgång på kakao – priset toppar nu 9000 USD

Kaffepriserna stiger på lågt utbud och stark efterfrågan

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanGuldpriset når nytt all time high och bryter igenom 2300 USD

-

Nyheter4 veckor sedan

Guld toppar 2200 USD per uns

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanLundin Mining får köprekommendation av BMO

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanVertikal prisuppgång på kakao – priset toppar nu 9000 USD

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanKaffepriserna stiger på lågt utbud och stark efterfrågan

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanCentralbanker fortsatte att köpa guld under februari

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHur mår den svenska skogsbraschen? Två favoritaktier

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanKakaomarknaden är extrem för tillfället